Getting The Mortgage Investment Corporation To Work

Table of Contents8 Simple Techniques For Mortgage Investment CorporationFacts About Mortgage Investment Corporation RevealedAbout Mortgage Investment CorporationSee This Report on Mortgage Investment CorporationMortgage Investment Corporation for Dummies

Does the MICs credit scores committee testimonial each home loan? In many scenarios, mortgage brokers manage MICs. The broker needs to not act as a member of the credit committee, as this places him/her in a straight conflict of rate of interest given that brokers usually gain a compensation for placing the home mortgages.Is the MIC levered? The economic organization will certainly approve specific home mortgages owned by the MIC as safety for a line of credit scores.

Last updated: Nov. 14, 2018 Couple of investments are as useful as a Home loan Investment Firm (MIC), when it pertains to returns and tax advantages. Due to their corporate framework, MICs do not pay income tax obligation and are legally mandated to disperse all of their revenues to investors. In addition to that, MIC dividend payments are treated as rate of interest income for tax obligation purposes.

This does not suggest there are not threats, yet, generally speaking, no matter what the broader stock market is doing, the Canadian property market, especially major urban areas like Toronto, Vancouver, and Montreal carries out well. A MIC is a company developed under the policies set out in the Earnings Tax Act, Section 130.1.

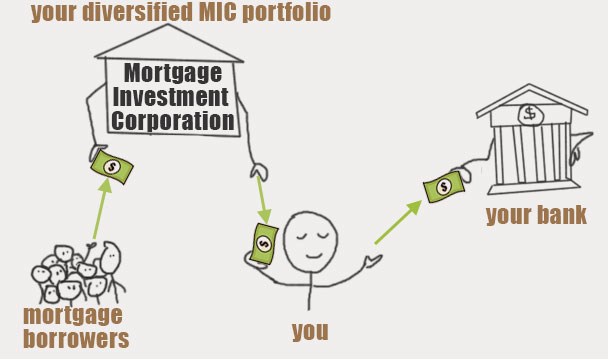

The MIC earns revenue from those home mortgages on passion costs and basic charges. The real appeal of a Mortgage Financial Investment Firm is the return it supplies financiers compared to various other set income investments - Mortgage Investment Corporation. You will certainly have no difficulty locating a GIC that pays 2% for a 1 year term, as government bonds are equally as low

The Of Mortgage Investment Corporation

There are stringent needs under the Earnings Tax Obligation Act that a company must satisfy before it certifies as a MIC. A MIC must be a Canadian company and it must spend its funds in mortgages. As a matter of fact, MICs are not allowed to handle or develop genuine estate home. That claimed, there are times when the MIC ends up having the mortgaged property because of repossession, sale agreement, etc.

MICs problem usual and preferred shares, releasing redeemable preferred shares to investors with a fixed dividend price. In many instances, these shares are considered to be "qualified investments" for deferred earnings strategies. Mortgage Investment Corporation. This is excellent for capitalists that purchase Home mortgage Financial investment Firm shares through a self-directed authorized retirement financial savings strategy (RRSP), signed up retirement income fund (RRIF), tax-free financial savings account (TFSA), postponed profit-sharing strategy (DPSP), registered education cost savings plan (RESP), or registered disability cost savings strategy (RDSP)

The Greatest Guide To Mortgage Investment Corporation

And Deferred Plans do not pay any kind of tax obligation on click here for more the interest they are approximated to obtain. That stated, those that hold TFSAs and annuitants of RRSPs or RRIFs might be hit with specific charge tax obligations if the financial investment in the MIC is taken into consideration to be a "banned investment" according to copyright's tax obligation code.

They will certainly guarantee you have actually located a Home mortgage Financial investment Company with "qualified financial investment" condition. If the MIC qualifies, check over here it could be very valuable come tax obligation time given that the MIC does not pay tax obligation on the passion income and neither does the Deferred Strategy. Much more broadly, if the MIC falls short to meet the demands laid out by the Earnings Tax Act, the MICs revenue will certainly be exhausted before it gets distributed to shareholders, decreasing returns substantially.

Many of these dangers can be minimized though by talking to a tax expert and investment representative. FBC has worked exclusively with Canadian local business proprietors, business owners, financiers, farm operators, and independent contractors for over 65 years. Over that time, we have assisted 10s of thousands of clients from across the nation prepare and file their taxes.

Facts About Mortgage Investment Corporation Revealed

It shows up both the real estate and stock exchange in copyright are at all time highs Meanwhile returns on bonds and GICs are still near record lows. Also money is shedding its appeal since power and food prices have actually pressed the rising cost of living price to a multi-year high. Which begs the concern: Where can we still find value? Well I think I have the solution! In May I blogged regarding checking into home loan financial investment corporations.

If passion rates increase, a MIC's return would additionally increase due to the fact that higher home mortgage prices suggest more earnings! Individuals that buy a mortgage financial investment firm do not own the realty. MIC financiers article merely earn money from the excellent position of being a lending institution! It resembles peer to peer financing in the united state, Estonia, or other components of Europe, other than every car loan in a MIC is protected by actual property.

Numerous tough working Canadians that want to purchase a home can not get home loans from traditional banks because perhaps they're self employed, or don't have a well-known credit scores history. Or maybe they want a brief term funding to establish a big residential property or make some remodellings. Financial institutions have a tendency to ignore these potential debtors due to the fact that self used Canadians don't have steady incomes.